Where Have All the Boxes Gone

In recent years, the retail industry has been abuzz with feverish talk of the Amazon effect, the retail apocalypse, and the end of brick and mortar. Despite the hype, small-shop leasing has stayed on pace year over year, while costs have continued to increase for landlords and tenants alike. Tenant mixes are shifting in centers to service and experience-based business, but one thing remains constant: Businesses continue to desire good real estate with visibility, access and parking so they can attract customers. The fundamentals of our business hold true over time and tenants consistently seek sound real estate choices to separate themselves from their competitors. However, we cannot fully escape the doom and gloom surrounding the dynamic landscape of the box world.

From 2016 to 2018, the negativity in the retail world at times was crushing. Every day another retailer was filing for bankruptcy, closing over 100 locations, or falling prey to Amazon’s insatiable appetite to acquire additional retailers. It was easy to grow pessimistic about the situation. This period was an equally scary time for power center owners; many were losing the bulk, or all, of their net-operating income with the loss of their anchor(s), a number of whom have been unsuccessful in finding replacement tenants. The retail industry had just jogged off its hangover from 2007-2008, and now the picture looked worse than before. After facilitating multiple medical deals, I remember telling my wife, “I should have been a damn dentist,” unwittingly acknowledging the very beauty underlying in the marketplace. Tenant types change and good landlords are creative problem solvers.

Altogether, the market has been fraught with challenges, but change is on the horizon. At the end of 2018, my team had a meeting with one of the top five largest real estate investment trusts. The feedback was a bit surprising: box leasing was steady. While growth was slow, with innovative approaches to addressing vacant units and expanding market segments, this REIT was finding tenants and backfilling space. What was more surprising to hear was that it was helping online retailers establish brick-and-mortar locations throughout the country.

More recently, during a tenant interview with a growing regional fitness chain, we were told the tenant was beginning to have trouble finding good boxes for its concept. Furthermore, this tenant now is exploring the need to develop ground-up to meet its expansion plans. Was this another positive signal in the marketplace? For many box tenants that have weathered the storm or are newly coming to market, the recent doom and gloom appears to have proven itself an opportunity.

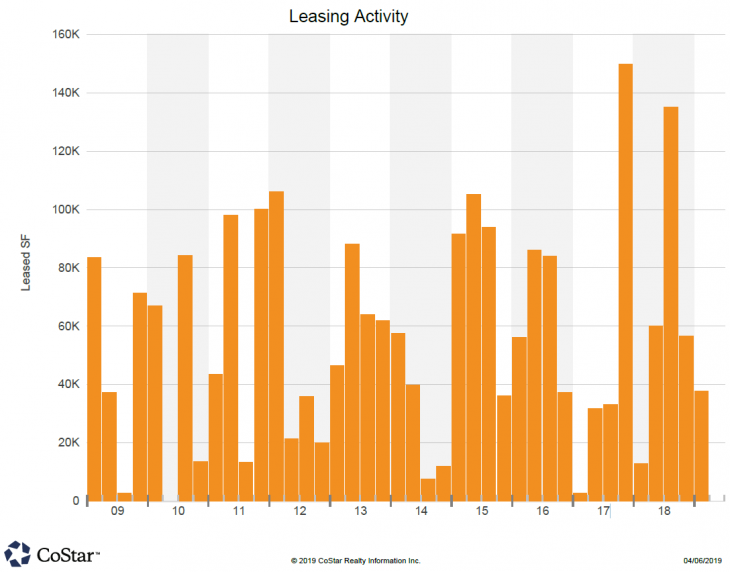

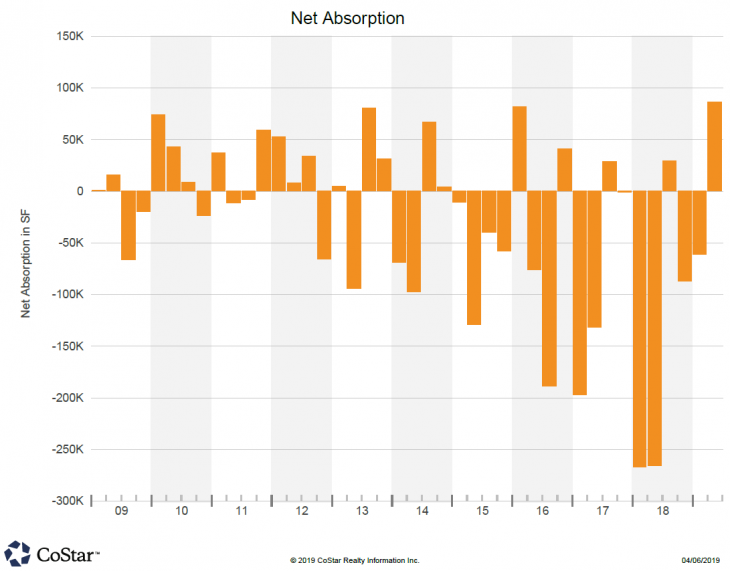

“Many of the box transactions we see today are existing tenants who are performing well in the market, but looking to improve the quality of their real estate,” said Blake Larson of Legend Retail Group. “Additionally, the vacancy has driven the rents lower and has provided many of these groups an opportunity to negotiate better leases.” A look at CoStar’s analytics for boxes from 20,000 to 100,000 square feet throughout the Front Range shows box leasing dropped off significantly in 2017. However, leasing is picking up, with some rather large spikes in fourth-quarter 2017 and then again in third-quarter 2018, bringing overall activity back to a historical pace. Readers might be quick to point out that much of the leasing activity in the last 18 months has been due to tenants relocating. It is important to note that absorption has been progressing over the last four quarters, and hopefully peaked in the first and second quarters of 2018. Reviewing the last year, CoStar’s analytics show signs of hope. Negative absorption is trending positively for landlords, and as of the date of this article, there is positive absorption for the second quarter.

A look at CoStar’s analytics for boxes from 20,000 to 100,000 square feet throughout the Front Range shows box leasing dropped off significantly in 2017. However, leasing is picking up, with some rather large spikes in fourth-quarter 2017 and then again in third-quarter 2018, bringing overall activity back to a historical pace.

Are we out of the woods yet? Not by a long shot. Solving the breakdown of the box market requires an all-hands-on-deck approach. There are fewer and fewer concepts coming to market in this tenant segment and the costs associated with backfilling these large vacancies are high. Landlords need to proactively consider the quality of their real estate and, depending on relative value, consider nontraditional tenant options for backfills of poorly located projects. Saturation also must be considered, as there are a finite number of budget gyms and food courts that can function sustainably in the market at any given time.

Ten-year retail net absorption for the metro area

Box vacancies impact owners and developers, but also the community at large. When the anchors of shopping centers fade away, the impact on the adjacent shop tenants often is devastating. More often than not, smaller tenants are “mom-and-pop” operators running family owned or independent businesses that are faced with an impossible decision: tough it out in a vacant center or pay 30% more rent with astronomical build-out costs.

The current state of the market is not what it was when these projects originally were built. There are a number of realistic and functional actions that can be taken to facilitate growth that adjusts for today’s landscape and consumer demand. For example, the aid of local governments working with owners and developers to adjust zoning to accommodate different uses would be very beneficial for these small shop tenants and owners. Retrofits for large boxes need to be encouraged. Considerations for these market changes need to be realistic and executable. The possibility of allowing residential density where these tenants once occupied also could be an interesting solution. As the market continues to be in flux, it poses both challenge and opportunity for the industry to elevate our game and think outside the box.